Walking into a real estate property transaction without understanding the language is like arriving in a foreign country without a map. Real estate terminology explained clearly can mean the difference between a confident negotiation and a costly misunderstanding. Whether you're buying your first home or selling a long-held property, the words in your contract carry real weight. This guide cuts through the property jargon to give you the clearest, most practical foundation possible, covering financial terms, contingencies, escrow, and closing so you can move forward with clarity and purpose.

Table of Contents

- Key Takeaways

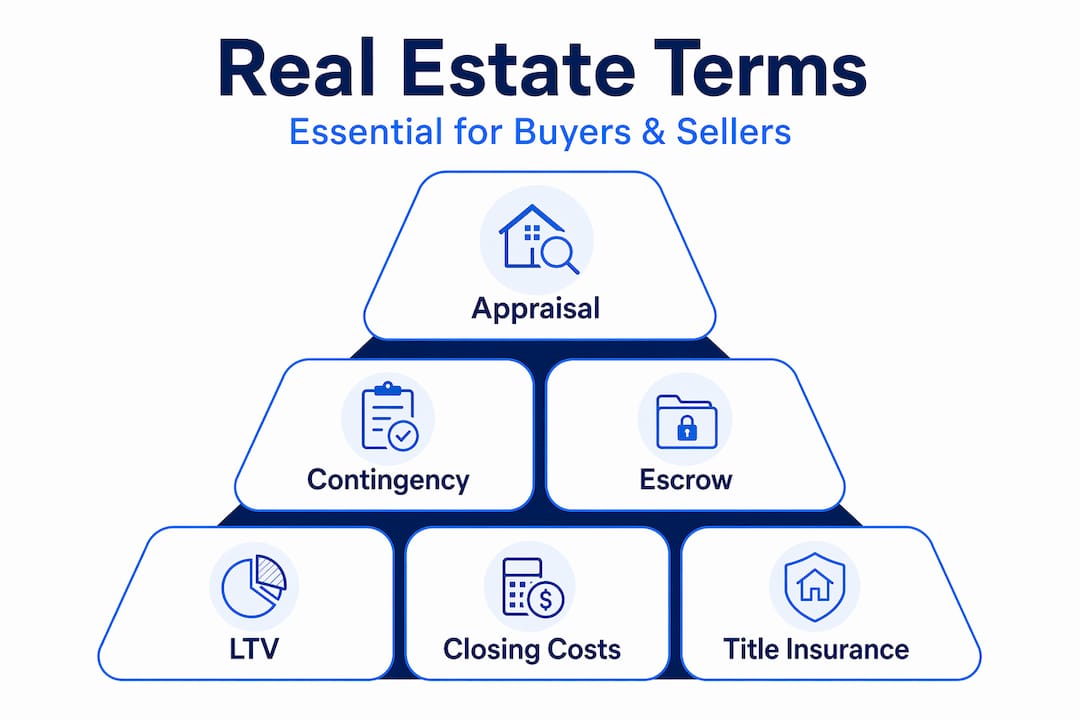

- Key financial terms you need to know

- Purchase contracts and contingencies

- Escrow, title insurance, and how they protect you

- Other commonly used real estate terms

- My perspective on what buyers consistently miss

- How Pacificisland guides you through every term

- FAQ

Key Takeaways

| Point | Details |

|---|---|

| Earnest money is time-sensitive | Deposits of 1% to 3% must typically be delivered within 1 to 3 business days after offer acceptance. |

| LTV ratio shapes your loan terms | An LTV at or below 80% lets you avoid PMI and often secures a better interest rate. |

| Contingencies protect your deposit | Buyer contingencies allow contract cancellation without penalty when specific conditions are unmet. |

| Closing costs add up quickly | Budget for 2% to 6% of the purchase price on top of your down payment for closing costs. |

| Escrow protects both parties | A neutral escrow holder cannot release funds without mutual consent or a court order. |

Key financial terms you need to know

Money is where confusion hits hardest. Before you sign anything, you need to understand exactly what you're committing to financially, and what happens if things don't go according to plan.

Earnest money

Earnest money is your good-faith deposit, the amount you put down to show a seller you're serious. Deposits typically range from 1% to 3% of the purchase price, and they must be delivered to escrow within a specified time frame, generally one to three business days after your offer is accepted. On a $1 million Maui property, that's $10,000 to $30,000 placed into escrow before you've even had an inspection. Some contracts will have another additional deposit that is made generally after the J-1 inspection expiration.

It's worth knowing that earnest money is only forfeited if a buyer defaults outside of valid contingencies. Walk away within a protected contingency window and your deposit comes back to you. Walk away without one and it's gone. There is no federal minimum or maximum amount either. Earnest money amounts are governed entirely by state law and the contract you negotiate.

Loan-to-value ratio (LTV)

LTV is the percentage of a property's value you're borrowing. If you put 20% down on a $500,000 home, you borrow $400,000. That gives you an 80% LTV ratio, which is the standard threshold to avoid Private Mortgage Insurance. Go above 80% LTV and most conventional lenders will require PMI, an additional monthly cost that protects the lender, not you.

LTV also directly affects your interest rate. Lower LTV leads to better rates because lenders price for risk at every tier. You can use a mortgage calculator to run the numbers and see exactly how your down payment affects your long-term costs. One option some lenders offer is lender-paid PMI, where the insurance cost is folded into a slightly higher interest rate instead of showing up as a separate monthly charge.

Closing costs

Closing costs cover everything from lender fees and title insurance to government recording charges and prepaid taxes. They typically range from 2% to 6% of the purchase price. On a high-value property, that number can be significant. Most people budget for the down payment and forget about closing costs entirely until the final week.

Pro Tip: Most closing costs are not tax deductible. Only select items like mortgage points may qualify under specific IRS criteria, and they cannot be double-counted with other deductions. Talk to a tax professional before assuming any savings.

| Cost Item | Typical Range | Tax Deductible? |

|---|---|---|

| Mortgage points | 0.5% to 2% of loan | Yes, if IRS criteria met |

| Title insurance | $500 to $3,500+ | No |

| Lender origination fee | 0.5% to 1% of loan | No |

| Prepaid property taxes | Varies by locale | Possibly, in future years |

| Recording fees | $100 to $500 | No |

For Maui-specific buyers, the typical closing costs in Maui carry their own nuances worth understanding before you reach the table.

Purchase contracts and contingencies

A residential purchase agreement is far more than a formality. It's a living document that defines your rights, your timelines, and your exit options. Understanding its structure before you sign is the single most protective thing you can do. The Hawaii Purchase Contract has many contingencies under which a buyer can cancel under if they choose. Working with a Buyer Representative who understands the contract and can negotiate on your behalf is important.

Here are the most common contingencies you'll find in a standard residential purchase contract:

- J-1 Inspection contingency: Gives you the right to have the property professionally inspected and to negotiate repairs, request credits, or walk away for any reason if the property is not acceptable

- M-1 Condominium document contingency: Gives you the right to review the HOA information, bylaws, minutes, and financials and decide to walk away if the information is not acceptable

- Financing contingency: Protects you if your loan is denied or the terms change materially before closing. This is not automatic. It only applies if it's written into the contract.

- Appraisal contingency: If the home appraises below the agreed purchase price, this contingency lets you renegotiate or exit without penalty.

Waiving contingencies can make your offer more competitive in a hot market, but it exposes you to losing your full earnest money deposit if you cannot close for any reason outside the contract.

Pro Tip: A signed offer that has been accepted may constitute a binding purchase contract, even if the document is labeled simply as an "offer." Never treat an offer as informal or reversible once both parties have signed.

Keep close track of contingency deadlines. Missing a deadline can inadvertently waive your protections, even if you intended to use them. Your agent should be tracking these dates alongside you and informing you of your rights within the contract. Contingencies in the Hawaii purchase contract expire whether or not they are signed off on. For example, as a buyer your inspection period ends per the dates and timeline in the contract whether or not you sign off to approve it.

Escrow, title insurance, and how they protect you

These two concepts often get lumped together, but they serve distinct purposes. Knowing the difference can prevent serious financial exposure.

Escrow is a neutral holding arrangement managed by a third party, often a title company, escrow company, or attorney depending on your state. When you submit your earnest money deposit, it goes into escrow, not directly to the seller. Escrow prevents premature fund release and protects both parties throughout the transaction.

Here's what makes escrow particularly important to understand:

- Escrow holders are legally neutral. They follow the contract's instructions, not the preferences of either party.

- Escrow holders cannot release funds without mutual written agreement from both buyer and seller, or a court order. This protects you, but it also means disputes can stall for months.

- Escrow closes when all conditions of the sale are met, funds are transferred, and ownership officially changes hands.

Title insurance is separate. A title search reviews public records to confirm the seller has clear, legal ownership of the property. Title insurance then protects you against claims that weren't found during that search, things like undisclosed liens, ownership disputes, or clerical errors in past deeds.

There are two types. A lender's policy protects the mortgage company. An owner's policy protects you. Both are typically purchased at closing, and skipping the owner's policy is a risk most real estate professionals strongly advise against. In Hawaii, where property history can include complex land tenure systems dating back centuries, a clean title search is not something to take lightly.

Other commonly used real estate terms

Real estate language extends well beyond the financial mechanics. These are the terms you'll encounter regularly throughout your transaction.

Appraisal is an independent assessment of a property's market value, conducted by a licensed appraiser. Lenders require it to confirm they are not lending more than a home is worth. The appraisal and the listing price are not the same thing.

Underwriting is the lender's process of verifying your financial profile before approving a loan. The underwriter reviews income, credit, assets, and the property itself. It's the step between "pre-approved" and "cleared to close."

Mortgage broker versus mortgage lender: a broker shops multiple lenders on your behalf. A lender is the institution that actually funds the loan. You can go directly to a lender or work through a broker, and each has trade-offs worth discussing with your advisor.

Here's a quick comparison of the most common loan types you'll encounter:

| Loan Type | Minimum Down Payment | LTV Allowed | Key Feature |

|---|---|---|---|

| Conventional | 3% to 20% | Up to 97% | Flexible; PMI required above 80% LTV |

| FHA | 3.5% | Up to 96.5% | Lower credit score threshold |

| VA | 0% | 100% | Available to eligible veterans and military |

| USDA | 0% | 100% | Rural and suburban areas only |

Beyond the purchase price, owning property comes with ongoing costs that buyers sometimes underestimate:

- HOA fees: Monthly or annual assessments for shared amenities and community maintenance.

- Property taxes: Calculated annually based on assessed value and local tax rates.

- Homeowner's insurance: Required by lenders and covers damage or liability.

- Special assessments: Occasional charges for large community improvements like roof replacement in a condo association.

Understanding these terms before you reach the closing table gives you the full picture of what homeownership truly costs, not just what you pay on signing day. For a full walkthrough of the buying process in Maui, Pacificisland has a detailed resource worth reading alongside this guide.

My perspective on what buyers consistently miss

I've sat across from buyers at every stage of experience, from first-time purchasers to seasoned investors, and the same blind spots appear again and again.

Slow down and make sure you read the contract and ask questions and know your rights and responsibilities within the purchase contract. Communicate with your agent throughout the escrow so your agent can be your advocate. Hire the right professionals to get more information when it is needed. Do you have questions about termites, roofing, or septic systems? Connect with the right professionals to get the best information during your contingency periods.

What I've learned is this: understanding real estate terminology isn't just about vocabulary. It's about knowing your exit options before you need them. A financing contingency you don't use is free insurance. A contingency you never added is a door that was never there.

Earnest money disputes are another area people don't think about until they're in one. When a transaction falls apart and both parties disagree on who gets the deposit, the escrow holder is legally stuck. They cannot move the money without mutual agreement. The dispute can sit for months, sometimes requiring legal action to resolve. The way to avoid this is to understand your contract terms before you're emotionally invested in the outcome.

My honest advice: read your purchase agreement carefully before you feel rushed. Ask your agent to walk you through every contingency, every deadline, and every condition. That conversation, had early, changes everything.

— Mark

How Pacificisland guides you through every term

At Pacificisland, clarity is not a courtesy. It's the foundation of every client relationship. Heidi Dollinger and Mark Janes have helped buyers and sellers through complex transactions across Maui and the surrounding islands, explaining not just what a term means, but why it matters in the specific context of your property and your goals.

When you're ready to explore available properties, you can browse the current listings in Maui and begin connecting the terminology you've learned here to real homes and real opportunities. To understand the depth of experience behind every transaction Pacificisland manages, visit the about the team page and discover the legacy of service that defines this practice.

Reach out directly when you're ready. The conversation costs nothing, and the clarity it brings is worth a great deal.

FAQ

What is earnest money in real estate?

Earnest money is a good-faith deposit made by the buyer after an offer is accepted, typically 1% to 3% of the purchase price. It is held in escrow and returned to the buyer if the contract is canceled within a valid contingency period.

What does LTV mean for a mortgage?

LTV, or loan-to-value ratio, is the percentage of a property's value you are borrowing. An LTV at or below 80% typically avoids PMI and qualifies for better interest rates from most conventional lenders.

What are real estate contingencies?

Contingencies are conditions written into a purchase contract that allow a buyer to cancel the agreement without penalty if those conditions are not met. Common types include inspection, financing, and appraisal contingencies.

What is the difference between escrow and title insurance?

Escrow is a neutral holding arrangement that protects funds during a transaction, while title insurance protects the buyer against ownership claims or defects discovered after closing. Both are distinct and both serve important protective functions.

Are closing costs tax deductible?

Most closing costs are not tax deductible. Only specific items like mortgage points may qualify under IRS rules, and they cannot be claimed alongside other deductions for the same expense. Consult a tax professional to confirm what applies to your situation.